Banks That Accept ITIN Numbers, this Navigating the U.S. banking system as someone who has an Individual Taxpayer Identification Number (ITIN) instead of a Social Security Number (SSN) can feel complex—but it absolutely doesn’t have to be impossible. In this guide, we’ll explore how banks that accept ITIN numbers operate, what you should know before applying, how to pick the right institution, and some of the most common hurdles you’ll face (and how to clear them). My goal is to help you approach this like a seasoned financial pro—giving you expert insight in a friendly, accessible tone.

What Is an ITIN—and Why It Matters for Banking

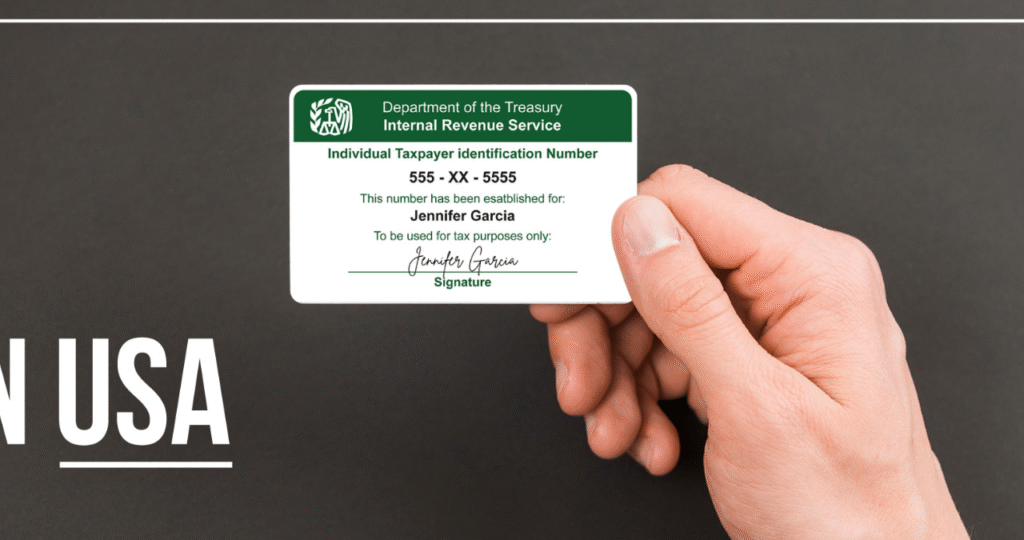

An ITIN is a tax processing number issued by the Internal Revenue Service (IRS) for individuals who are required to have a U.S. taxpayer identification number but are not eligible for an SSN.

When it comes to banking, the significance of the ITIN is this: many U.S. banks typically ask for a valid SSN to open accounts, especially for residents or citizens. But people who don’t have SSNs—such as non-residents, recent immigrants, dependents, or people working in the U.S. under certain visa status—can often use an ITIN instead.

Why does banking with an ITIN matter? Having an account in a U.S. bank gives you access to everyday financial tools—direct deposits, debit cards, online bill pay, building credit history, and more. Without that banking base, you may end up relying on cash or alternative services that cost more or offer fewer protections.

In short: the ITIN is your key to unlocking more of the U.S. financial system—even if you don’t have an SSN.

Who Can Use an ITIN to Open a Bank Account

If you’re wondering whether you can open a bank account using an ITIN, here are the typical situations in which this applies:

First, non-U.S. citizens or non-residents who live or work (even temporarily) in the U.S. often use an ITIN because they need to file taxes but don’t qualify for an SSN.

Second, immigrants, visa holders, dependents of visa holders, or individuals who may not have work authorization but still must report income or have banking needs—these are all scenarios where using an ITIN is common.

Third, even residents without full eligibility for SSNs may use ITINs for banking and tax purposes. The important part is that the bank accepts the ITIN as a form of identification or tax identification.

It’s important to note: having an ITIN doesn’t mean full equivalence to an SSN. An ITIN does not authorize work in the U.S., for example.

So if you fall in one of those groups and you don’t have an SSN, you’re in the right space to explore “banks that accept ITIN numbers”.

What Requirements Banks Commonly Have When Accepting ITINs

Opening a bank account when using an ITIN instead of an SSN often means you’ll need to meet a few extra documentation criteria. Here’s a breakdown of what banks usually ask for—and what you’ll want to prepare in advance.

1. Valid Identification

You’ll likely need a government-issued photo ID: this could be a passport, foreign driver’s license, a U.S. state ID, or driver’s license (if applicable). Some banks will accept more than one form of ID if one doesn’t include all the required info.

2. Proof of U.S. Address

Even non-residents often must provide a U.S. address (or at least a valid one they can link to). This might be a utility bill, lease agreement, bank statement, or other document showing your name and U.S. address.

3. Your ITIN

You’ll of course need the ITIN itself, issued by the IRS, to fill in the tax ID portion of the banking application. Some banks make it clear: yes, we accept ITIN instead of SSN.

4. Minimum Deposit or Account Opening Conditions

Some banks may require a minimum opening deposit or certain conditions (like you must visit a branch in person, or you need additional documentation if you open online).

5. In-Branch Visit (Sometimes)

While some banks allow online applications, many banks that accept ITINs may require you to visit a branch in person. This is especially common for non-citizens or non-residents.

6. Credit or Other Financial History

Depending on the account type you’re opening (checking, savings, or even credit cards), the bank may ask for additional verification of financial stability or history. This is less about the ITIN and more about standard risk assessment.

Benefits of Opening an Account with an ITIN

Let’s talk about why it’s a good move. If you’re using an ITIN to open a bank account, you get multiple advantages.

Financial Access

You gain access to everyday banking services: checking and savings accounts, debit cards, online banking, receiving payments, securely withdrawing funds, and paying bills. These are standard but powerful. For non-citizens or recent immigrants, this can be a major step forward.

Build Credit History

Although an ITIN by itself doesn’t guarantee credit, having a bank account can be the first step toward establishing credit in the U.S. system. Some banks report account activity to credit bureaus, and over time, this can open doors such as car loans, home loans, or other financing. Security and Convenience

Rather than keeping cash, relying on expensive remittance services, or dealing with less-regulated financial services, a bank account offers FDIC-insured deposits (in most U.S. banks), security, and the convenience of online/mobile banking.

Integration into U.S. Financial Life

If you’re living in the U.S., working, studying, building a future here, having a bank account brings you into the mainstream financial infrastructure. It helps with direct deposit, automatic payments, budgeting tools, and more.

Challenges and Things to Watch Out For When Using an ITIN

While the path is clear, there are a few pitfalls and caveats you should be aware of when you use an ITIN to open a bank account.

Limited Bank Options

Not every bank accepts ITINs or is equally friendly to non-resident/non-citizen applicants. Online account opening might not always be available. Some banks make it very clear they only accept SSNs for online openers. So you’ll want to research banks that explicitly mention they accept ITINs.

In-Branch Requirement

As mentioned, many banks will require you to physically go to a branch, present ID in person, etc. For non-residents or if you’re applying from abroad, this may complicate matters.

Higher Minimums or Stringent Conditions

When opening remotely or with an alternative ID, you might face higher minimum deposits, more verifications, or stricter criteria.

Potential Language/Documentation Barriers

If English is not your first language, or you hold foreign ID documents, you may need extra time to prepare documents and ensure they meet the bank’s verification requirements (translated documents, notarized, etc).

Not automatically eligible for All Services

Opening a basic checking or savings account with an ITIN is usually possible, but applying for credit cards, loans, or other financial products may still require an SSN, credit history, or other documentation. So while you can open accounts, some services might be limited at first.

How to Choose the Right Bank When You Have an ITIN

Since you’re working from a slightly different normal (than someone with an SSN), choosing the right bank becomes extra important. Here are the criteria and questions to ask—and things I’d recommend you weigh like an expert.

1. Confirm They Accept ITINs

First and foremost: check whether the bank explicitly says they accept an ITIN instead of an SSN, and note whether the application must be in-branch or can be online. Many banks list this on their website, or you can call a branch to ask. For example, some mainstream banks do accept ITINs.

2. Fees and Account Minimums

Even if the bank accepts ITINs, look at the fee structure: monthly maintenance fees, minimum deposit requirements, ATM access, foreign transaction fees, etc. One decent bank option may cost less in hidden fees than another fancy bank that has higher hurdles.

3. Branch & Online Access

If you are in the U.S., having a nearby branch may help (especially to get started). If you’re abroad or remote, a strong online/mobile banking capability is essential. Evaluate whether the bank’s online application process supports ITIN holders.

4. Additional Services

Will the bank let you open a savings account, debit card, and maybe send/receive international wires? If you plan to build credit, does the bank offer credit cards later? Does it support online bill pay, mobile deposits, and ATM network access?

5. Language & Customer Support

If English is not your first language, check whether the bank offers multilingual support or documentation in your preferred language. Also consider whether the bank’s staff is familiar with non-resident/non-citizen clients.

6. Reputation & Security

Check that the bank is FDIC-insured (or NCUA-insured if a credit union), has good online security, and has reviews from customers. For non-citizen clients, it’s particularly important to work with a bank that treats your account professionally and doesn’t apply hidden hurdles.

7. Future Growth Capability

Think ahead: in a year or two, when you’ve built a banking history, will you be able to apply for credit or loans? Some banks might limit services for ITIN-holders initially, so choosing one that offers upward mobility matters.

Example Banks That Accept ITINs and What They Offer

Here are a few banks and institutions that have proven track records of accepting ITINs. While this list is by no means exhaustive, it gives you a solid starting point.

- Bank of America: This major bank mentions support for international students or professionals without SSNs, offering account opening, debit cards, mobile banking, etc.

- Chase Bank: Known to allow account openings for non-residents who can supply an ITIN, though in-branch visits may be required.

- Wells Fargo: One of the larger banks that accepts ITIN for checking account openings (with ID/proof of address), as displayed in their identification requirements.

- Amplify Credit Union: A credit union example that explicitly lists how an ITIN can be used to open account types, highlighting the steps and documentation required.

Each of these institutions has slightly different rules, so you’ll want to call ahead and confirm for your specific branch and your situation (residence status, visa status, etc).

Step-by-Step: How to Open a Bank Account with an ITIN

Let’s walk through a typical process step-by-step (adapted for someone who has an ITIN and maybe no SSN). This gives you a roadmap you can follow.

Step 1: Gather Your Documentation

- Valid photo ID (passport, driver’s license, state ID, or equivalent)

- Your ITIN (issued by IRS)

- Proof of U.S. address (utility bill, lease agreement, bank statement, etc.)

- Possibly proof of foreign status (if non-resident) or visa/entry record

- Initial deposit amount (some banks have a minimum)

Step 2: Choose the Bank and Account Type

Decide whether you want a checking account, a savings account, or both. Based on your needs (daily transactions vs savings), select a bank that accepts ITIN and offers the features you want.

Step 3: Visit the Branch or Apply Online

If applying in-branch: bring your documents, speak to a banker, and explain that you have an ITIN and not an SSN. Ask about any special forms they might require.

If applying online, check that the bank’s online system allows ITIN holders. Upload scanned documents as required. Be ready for potential follow-up verification.

Step 4: Submit Application & Deposit Funds

Fill out the account opening form and submit the required documents. Make your initial deposit (if required).

Ensure that the bank records your ITIN in the “Tax ID” or “Social Security Number” field (or alternative field) properly.

Step 5: Activate & Use Account

Once approved, you’ll get your debit card and online banking setup, and you can fund the account. Make small initial transactions to test everything works (ATM withdrawal, debit purchase, deposit).

Step 6: Monitor Account & Build History

Use the account responsibly: avoid overdrafts, keep a positive balance, use it for direct deposits if possible, and pay any bills. Over time, this builds your banking history and helps with credit and additional services.

Step 7: Upgrade When Ready

After you’ve maintained your account and built trust with the bank, check whether you’re eligible for other products—such as credit cards, loans, or higher-tier savings accounts. If you later obtain an SSN, you may transition the account or add it.

Common Questions and Myth-Busting

Let’s clear up some of the most frequent questions or misunderstandings people have when they’re looking for banks that accept ITIN numbers.

“Can I open the account entirely online with an ITIN?”

Yes—and sometimes no. Some banks allow online account opening with an ITIN, but many still require an in-branch visit, especially for first-time non-resident applicants. The key is to verify with the bank ahead of time.

“Will the bank treat me differently because I used an ITIN instead of an SSN?”

Possibly. Some banks may impose stricter documentation requirements, limit certain services initially, or categorize the account differently. But having an ITIN doesn’t mean you get inferior service—it means you may need slightly more reps or deeper documentation.

“Does having an ITIN automatically build a credit history?”

Not automatically. Having a bank account is an important step, but building credit often requires credit products (credit cards, loans, and timely payments) being reported to credit bureaus. Some banks with ITIN-friendly policies also offer credit products over time.

“Am I eligible for all types of accounts (business accounts, savings, checking) with an ITIN?”

Many personal checking and savings accounts are available with ITINs, but business accounts or more complex financial products may have additional requirements (e.g., business registration, EIN, SSN, residency).

“What if I’m abroad or I don’t have a U.S. address?”

Opening U.S. bank accounts from abroad or without a U.S. physical address is more challenging. Some banks or international banking services facilitate this, but often with higher minimums or stricter documentation. Strategic Tips to Maximize Your Banking Experience with an ITIN

Here are some pro-tips—things you won’t always read on the front page of a bank’s website—but that can make your banking experience much better when using an ITIN.

- Choose a branch you can visit (if in the U.S.)

- Visiting in person often simplifies the process and helps build rapport with the bank staff. If you walk in and say you have an ITIN and need to open an account, the staff may guide you more smoothly.

- Prepare your documents carefully.

- Scanned copies should be clear, combine translations if needed, and ensure your proof of address is recent (within the last 30-60 days). Turn up early if in-branch with all originals.

- Ask about fees and minimums upfront.

- Sometimes banks have hidden fees (monthly maintenance, ATM surcharge, foreign transaction) that affect newcomers more. Make sure you know the full cost of the account.

- Start with a simple checking account.

- If you’re just getting into the banking system, open a basic checking account first, then gradually add savings or other products. This builds your track record.

- Use your account actively but appropriately.

- Deposit funds regularly, use the debit card, withdraw occasionally, and pay bills. Banks like to see activity (not inactivity) but also responsible behavior.

- Ask about future credit opportunities.

- When you open the account, ask: “After X months of good banking history, can I apply for a credit card or loan?” This sets a roadmap for you.

- Keep your ITIN documentation safe.

- Save your ITIN issuance letter, keep your passport/IDs current, and make sure you monitor your account for any unusual holds or issues.

- If you later receive an SSN, update your information.

- If at some point you become eligible for an SSN (for example, you work), update your bank with your SSN and request to merge or upgrade your account accordingly.

- Consider linked services (mobile banking, apps, alerts)

- Choose a bank whose digital services are strong, so you can manage from anywhere—especially helpful if you travel or are working across borders.

- Use the account to build your financial plan.

- Treat it not just as a place to store money, but as the foundation of a financial system: budgeting, saving, transactions, and credit path. The sooner you treat it seriously, the better your long-term outcome.

Real-Life Scenario: How This Works in Practice

Let’s imagine a person named Maria: she has moved to the U.S. on a visa, doesn’t yet have an SSN, but she obtained an ITIN because she needs to file taxes. Maria wants to open a checking and savings account to start building her financial foundation.

Step 1: Maria researches banks in her city. She calls a few branches and finds that Bank of America and Wells Fargo both mention they accept ITINs (Maria confirms the branch does).

Step 2: She gathers her documents: her foreign passport, visa, a utility bill with her name and U.S. address (apartment lease + light bill), and her ITIN letter. Also, she brings proof of initial deposit (say $100).

Step 3: She visits the bank in person. She lets the banker know she has an ITIN, wants a basic checking account, and is fine with the stated fees. The banker runs the application.

Step 4: The bank approves her account. She receives a debit card, sets up online banking, deposits funds, and uses the card for small transactions. She sets recurring deposits from her paycheck.

Step 5: Over a year, Maria uses the account responsibly: no overdrafts, uses the debit card monthly, and holds a positive balance. After 12 months, she asks the bank if she qualifies to apply for a credit card for ITIN holders. The bank provides a secured credit card option.

By the end of two years, she has a checking account, savings account, debit card, and a small credit card—all with an ITIN. This places her firmly within the U.S. banking system, helps reduce reliance on cash or informal financial services, and positions her well if she later obtains an SSN or wishes to apply for bigger loans (car, home, etc).

Why This Matters for You (Especially if You’re a Non-Resident, Immigrant, or Recently Arrived)

If you’re using an ITIN because you’re in a non-traditional residency/work scenario, here’s why adopting this banking strategy is especially important.

- You’re establishing your financial footprint in a new environment. Having a recognized bank account helps you integrate financially.

- You’re reducing vulnerability. When you rely on cash or non-bank methods, you often face higher costs, lower security, and fewer protections. A bank account gives you more stability.

- You’re preparing for future financial goals. Whether that’s a car purchase, starting a business, saving for a home, or someday getting an SSN, a banking base is core.

- You’re improving your independence and convenience. Direct deposit, online payments, and debit cards—these make life smoother and less dependent on others.

- You’re building trust with financial institutions. When banks see you as a responsible account-holder (even with an ITIN), they’ll be more open to offering you additional services.

Things to Double-Check Before You Sign

Before you commit, here are a few last checks I always suggest:

- Ask the banker: “Will my account remain okay if I’m a non-resident and have this visa/ITIN setup?”

- Verify the opening deposit amount and whether any maintenance fees are waived—some banks waive fees if you meet direct deposit or balance thresholds.

- Confirm how the bank treats ITIN holders in terms of credit card/loan eligibility later. Will your account history count?

- Ask about ATM networks and international access if you travel. Will your debit card work abroad? Are there foreign transaction fees?

- Understand how to upgrade your account if you later obtain an SSN (you don’t want to open a new account from scratch).

- Make sure your online banking setup is strong: mobile app, alerts, ability to view statements, and remote deposit if available.

- Ensure your communication preferences: are statements in English only? Are there multilingual support options if needed?

- Ask about FDIC insurance or equivalent protection. Even though most big banks are covered, it’s always good to confirm.

When Things Go Wrong: Troubleshooting Tips

Even with the best preparation, you might hit bumps. Here are some common issues and solutions.

Application Rejected Because of ID

If a bank rejects your application due to a foreign ID or proof of address, ask what the missing piece is. Often it’s a mismatch in name/address, an expired ID, or missing proof of U.S. address. Fixing the document and re-applying often works.

Online Application Doesn’t Accept ITIN

If the online form only asks for an SSN and doesn’t let you proceed with an ITIN, visit a branch or call the bank’s non-resident department. Some banks restrict online processes for non-citizen applicants.

Account Fees You Didn’t Expect

You may open the account and later discover maintenance fees (if you don’t meet certain conditions). To avoid this, ask about the fee waiver conditions (like $1,000 minimum balance or $500 monthly deposit) at the start.

Difficulty Upgrading to Credit or Loan

If the bank says you’re not eligible yet for credit because you don’t have an SSN, ask about what you can do: maintain an account for 12 months, use a secured credit card for ITIN holders, etc. Some banks have alternative pathways for ITIN customers.

Changing Residency/Obtaining SSN

If your status changes (you get an SSN or you move), contact the bank to update your account details, switch to new account tiers, or avoid penalties for outdated info. Don’t let outdated ID or status linger.

Future Outlook: Where This Trend Is Going

The good news is the trend is moving in a favorable direction: more banks are recognizing the value of offering services to ITIN holders and non-resident/new‐immigrant clients. Here are a few predicted developments:

- More “ITIN-friendly” banking products: We’re seeing more banks and credit unions explicitly marketing accounts for ITIN holders, with tailored onboarding and multilingual support.

- Better online and remote account openings: As digital banking evolves, banks or fintechs may streamline onboarding for ITIN holders with fewer branch visits needed. Some remote options are already being piloted.

- Increased credit access for ITIN holders: With more credit-reporting firms and banks offering alternative documentation tracking (including ITIN), people using ITINs might see better access to credit or loans in the future.

- Greater financial inclusion and awareness: As more immigrants, non-residents, and global professionals look to access U.S. banking, the financial industry may innovate in how to serve those with non-traditional ID or residency status.